Credit investing is a business of nuance — of measuring reward versus risk not just in spread terms, but in real return terms, liquidity terms, and behavioural terms. It’s about distinguishing today’s price from tomorrow’s value. And it requires not only an understanding of macroeconomic drivers, but also humility about what we can and can’t know in the short run.

At Cavalen, we focus on absolute yield, not just spread levels. When yields on investment-grade and selective high yield bonds offer meaningful income — and when that income is backed by resilient fundamentals — the investor is paid to wait. That’s a powerful position to be in, especially when policy and sentiment remain in flux.

Where Are We Now?

Today’s credit markets appear resilient — and in many respects, they are. Spreads have narrowed considerably from early April’s risk-off episode, when tariff headlines and geopolitical nerves created a temporary dislocation. The bounce-back since then has been orderly, helped by calm central banks, steady demand, and supportive technicals.

Fundamentally, the picture — particularly in European high yield — remains stable. Leverage metrics are still below long-term norms, and despite the rise in funding costs, many issuers maintain reasonable interest coverage ratios. The percentage of distressed bonds — those trading at deeply discounted prices or extremely wide spreads — has shrunk materially, suggesting that the market doesn’t anticipate a near-term wave of defaults.

Technicals continue to do much of the heavy lifting. With subdued net supply, steady inflows, and a backdrop of ongoing income accrual, there’s a persistent bid not just for high yield, but for credit more broadly. That helps explain why spreads remain compressed — though, from our perspective, not necessarily cheap.

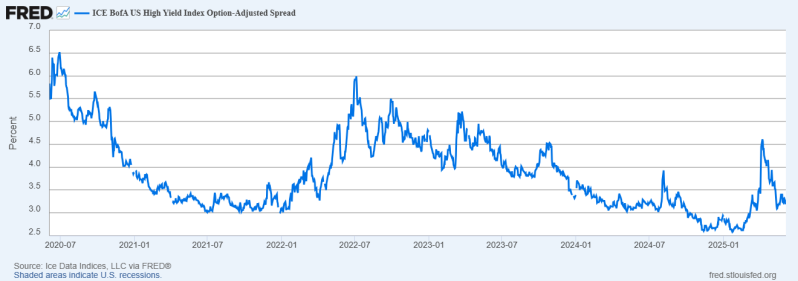

Chart: US High Yield Spreads remain near post-April lows despite recent volatility.

Source: ICE BofA via FRED, Federal Reserve Bank of St. Louis.

Valuations: A Measure of Complacency?

There’s a risk now that credit markets are leaning too heavily on these supportive technicals. When spreads are tight, it doesn’t mean risk is absent — just that it’s not being priced generously. Credit default swaps, corporate bond indices, and primary market reception all reflect a broadly optimistic outlook. That may prove justified. But we believe it’s prudent to acknowledge the potential for complacency.

It’s precisely during these periods — when everything feels calm — that we focus harder on our core principles:

- Know what you own

- Be paid for the risks you’re taking

- Don’t reach for yield when you’re already being well-compensated for patience

We continue to favour higher-quality bonds, defensively tilted portfolios, and select credits that we know extremely well — issuers we’ve followed for years, through multiple cycles, backed by deep research and active monitoring.

Opportunities Amid Complexity

This is not a call for alarm. There are still pockets of value — particularly in the new issue market, where concessions remain attractive in some deals. And idiosyncratic dislocations persist beneath the surface, offering opportunities for those with conviction and flexibility.

Even after the rebound, we still observe that issuer-level fundamentals matter more than ever. The dispersion that emerged earlier in the year hasn’t fully vanished — and in some cases, technical-driven rallies have papered over fundamental divergence. That creates pockets of opportunity for active managers willing to differentiate.

But this is a market to approach with care. In our view, absolute yields offer sufficient return potential, especially when balanced against risk. That doesn’t require heroic risk-taking — just sound underwriting, long-term thinking, and discipline.

What We’re Focused On

- Tracking credit issuance for signs of strain or stress pricing

- Monitoring liquidity conditions and dealer balance sheet capacity

- Evaluating policy shifts, particularly around tariffs and fiscal responses

- Remaining attuned to global fund flows and CTA positioning

- Avoiding areas of hidden leverage or false comfort

Final Thought

When the tide is in, as it feels today, we want to be positioned with strong swimmers — not reliant on the current. We’re happy to earn carry in high-quality credit, keeping dry powder for when value becomes more compelling.

At Cavalen, our edge is not prediction — it’s preparation.