The Calendar as a Signal: Exploiting Rebalancing Inefficiencies in Bond Markets

In markets defined by data and precision, it is often structure—not sentiment—that reveals the most consistent opportunities. One such structural inefficiency arises not from mispriced fundamentals or surprising macro releases, but from something far more mundane: the calendar.

These rebalancing flows are typically driven by large institutional investors such as global pension funds, sovereign wealth funds—including well-known entities like Norway’s Norges Bank—and multi-asset funds that follow fixed asset allocation rules.

A recent academic study from the National Bureau of Economic Research (NBER), titled “The Unintended Consequences of Rebalancing” by Harvey, Mazzoleni, and Melone, has quantified what many experienced investors have long suspected—that systematic, calendar-based rebalancing by large institutional investors creates predictable flows, and in doing so, opens the door to front-running and return drag. When billions of dollars shift into or out of bonds at regular intervals—often around month-end—the resulting market impact becomes measurable, and more importantly, exploitable.

The researchers modelled two common rebalancing approaches:

- a calendar-based strategy, where investors rebalance on the final trading day of each month, and

- a threshold strategy, which allows allocations to drift within bands before adjusting.

Their analysis showed that when equities outperform bonds, rebalancing leads to selling pressure in equities and increased bond demand. Conversely, when equities underperform, the flows reverse—providing upward pressure on stocks and reducing bond buying. The result? A 16 basis point decline in equity prices and a 4 basis point uplift in bond prices in the immediate aftermath—driven not by fundamentals, but by structural flows. These effects tended to fade within two weeks, underscoring that they carry limited informational content, but offer tactical opportunity.

Even more compelling, the researchers constructed a model portfolio that front-ran these flows using their signals. It achieved an annualised return of 9.9% over 1997–2023, with a Sharpe Ratio above 1, and performed especially well during periods of market stress—precisely when rebalancing volumes spike.

These patterns are not just academically interesting—they are monitored and sometimes front-run by hedge funds, tactical asset allocators, and fast-money traders who seek to exploit the price impact of predictable flows.

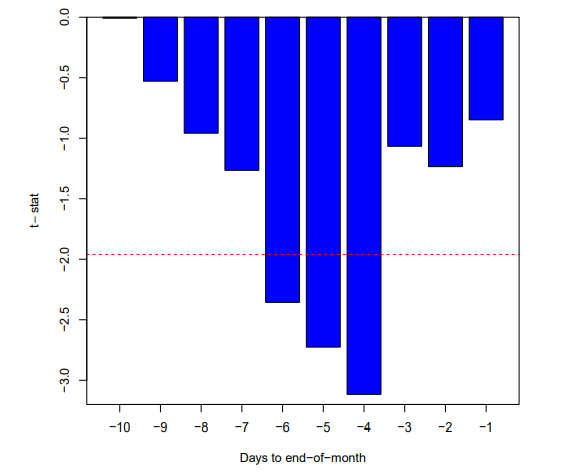

Figure 1 – Calendar Signals and End-of-Month Effect

This chart illustrates how predictable rebalancing flows influence market returns in the final days of each month. Equity performance relative to bonds becomes negatively predictable, with the effect strongest in the last four trading days. The pattern suggests that institutional investors often stagger trades across several sessions to avoid market disruption—creating opportunities for those who understand the signal.

Source: Harvey, C. R., Mazzoleni, M. G., & Melone, A. (2024). The Unintended Consequences of Rebalancing, NBER Working Paper No. 31957.

These are not isolated observations. Over time, we’ve developed a broader suite of tradeable models informed by flow dynamics and structural imbalances. These include, but are not limited to:

- Anticipated month-end rebalancing activity

- Supply and demand imbalances from intra-month issuance patterns

- Projected fund flows

- CTA positioning and potential inflection points

This technical framework does not require a view on growth, inflation, or central bank policy. Instead, it allows us to step into markets when flows—not fundamentals—dominate price action. In volatile environments, especially when traditional macro signals are clouded by noise, this structural edge can be particularly valuable.

We do not claim this inefficiency will persist forever. But market structure tends to evolve slowly. As long as large allocators continue to rebalance on set schedules, and as long as their behavior remains predictable, opportunities will remain for those with the discipline and tools to anticipate their actions.

The broader lesson is one we return to often: in a world crowded with forecasters, sometimes it pays to watch the flow. And when too many investors move at the same time, price is often an afterthought.

This article was written by Craig Veysey, Founder and Chief Investment Officer at Cavalen Asset Management.

Reference:

Harvey, C. R., Mazzoleni, M. G., & Melone, A. (2024). The Unintended Consequences of Rebalancing. National Bureau of Economic Research.