Markets are learning that patience, not timing, delivers value — and today’s yields still reward those who stay disciplined.

The Federal Reserve is widely expected to cut rates again today, following softer inflation prints and weaker employment data. Headline CPI remains near 3.0%, with core gradually trending toward 2½%, sufficient to justify another modest 25bp move. The ECB, by contrast, remains on hold as inflation sits closer to its 2% target after earlier rate cuts from a peak of 4.5% (Sep ’23) to 2.15%. In the UK, the Bank of England last reduced its Bank Rate to 4.00% in August, from a peak of 5.25% a year earlier.

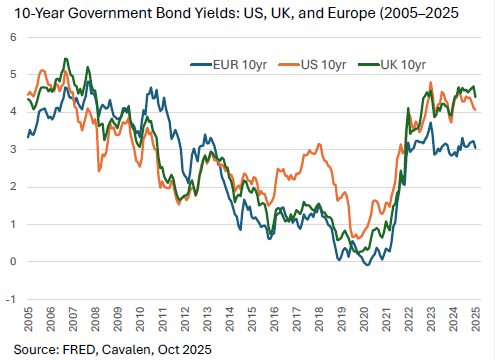

Over the past two years, both US Treasuries and UK gilts have traded around 5% yields at their peaks — with US 10-year yields reaching 5% in Oct 2023, but gilts around 4.9% this year. Since then, yields have eased to around 4.0% and 4.4%, respectively, still leaving long term bond investors with one of the most attractive starting points for high-quality fixed income in more than a decade.

Yields remain high even as confidence returns

Global bond yields have fallen from this year’s highs, but they remain far above the suppressed levels that defined the 2010s. The Bloomberg Global Aggregate yield is now about 3.4%, up sharply from a pandemic low near 0.9% — a structural reset that continues to reward patient bond investors.

- US 10-year: 4.0%

- UK 10-year: 4.4%

- German 10-year: 2.6%

Across markets, entry yield still explains most of total return — and today’s levels continue to offer a margin of safety. A 4–5% income stream compounds quietly but powerfully, particularly for those reinvesting in an environment still pricing policy uncertainty rather than complacency.

The comfort of cash

Money-market balances remain near record highs, around $7.4 trillion in the US, as investors wait for clarity. Yet each reinvestment cycle brings lower yields as central banks move deeper into easing. The comfort of cash may soon become an expensive form of caution.

At Cavalen, patience doesn’t mean inactivity. It means owning the right risks at the right prices — extending and reducing duration selectively across global markets and favouring quality credit while others sit in liquidity. The shift from restraint to accommodation rarely feels linear. Front-end yields may fall first, steepening curves and creating opportunities to add longer duration when value re-emerges.

Inflation and policy transition

- United States: CPI 3.0% y/y (Sept); Fed funds 4.00–4.25% after September’s cut — real policy rates remain mildly restrictive.

- United Kingdom: CPI 3.8% y/y (Sept); Bank Rate 4.00% after August’s move.

- Euro Area: CPI 2.2% y/y (Sept); ECB deposit rate 2.15%, following reductions from last year’s 4.5% peak.

Disinflation is broadening, yet policy is still tight in real terms — an unusual but constructive mix for bond investors. Historically, these transitions, when inflation cools before policy turns easy, have generated some of the best forward-looking risk-adjusted returns in fixed income.

Strategic bonds through the cycle

In recent weeks, gilts have outperformed Treasuries, with 10-year yields falling roughly 35 bps, helped by renewed fiscal credibility and steadier communication from policymakers ahead of the Autumn Budget.

For Cavalen, strategic bonds means flexibility through the cycle:

- Sovereigns vs credit: maintain core duration where valuation compensates; favour high-quality investment-grade for stability.

- Selective carry: identify value in BB and crossover credit, where refinancing risk is rising but spreads still reward conviction in specific credits.

- Geography & curve: rotate tactically as policy paths diverge and steepening creates opportunity.

Credit spreads remain tight — roughly 70–100 bps across major investment-grade markets — bringing all-in yields near 5% for quality issuers. These are not distressed levels, but they remain attractive for patient capital willing to earn carry while awaiting future dislocation. The latter is inevitable, but the timing is something that we can't be sure of.

The patience premium

This isn’t about calling the day of the pivot. It’s about owning value today so that compounding does the heavy lifting tomorrow.

Spreads may be narrow, but all-in yields on quality credit remain far above the norms of the past decade — a blend that rewards those who stay selective, liquid, and calm.

Patience, not optimism, is what compounds value. The patience premium is earned by investors who maintain exposure through the quieter middle of the cycle — harvesting income while others wait for perfect visibility.

| Theme | Current Setting | Cavalen View |

|---|---|---|

| Policy | Fed funds 4.00–4.25%; BoE 4.00%; ECB 2.15% | Real rates mildly tight — supportive for duration |

| Valuation | US 10-year 4.0%, UK 10-year 4.4%, Bund 2.6% | Lock in income at upper end of recent ranges |

| Inflation | US 3.0%, UK 3.8%, EA 2.2% | Disinflation broadening; patience rewarded |

| Credit | Spreads 70–100 bps; fundamentals solid | Prefer quality and liquidity; add selectively |

| UK gilts | Outperformed on fiscal credibility | Maintain moderate duration bias; monitor fiscal delivery |

Add comment

Comments